By Roger Chesley

Spare no tears for Advance America, Virginia’s largest payday loan operator. The company has now decided to flee the commonwealth before new, tougher regulations passed by the General Assembly begin next year.

You can bet the more than 80,000 Virginians who got payday loans, just in 2018 alone, from Advance America and similar companies aren’t taking out the hankies. These folks – down on their luck, struggling with health emergencies, or simply short on cash at the end of the month – are instead hoisting a single-digit salute to the South Carolina-based firm and its ilk.

It’s not a gesture of praise.

That’s because payday, car title and online lenders have so far enjoyed a very sweet deal in Virginia. They’ve reaped triple-digit, annual interest rates on loans to people who usually don’t realize the mess they’ve agreed to, until it’s too late.

Many customers then put good money after bad, taking out even more loans to settle up their accounts. All the while, the borrowers are racking up debt, fees and a jacked-up credit history.

With the Assembly’s blessing, payday loan companies set up shop in Virginia in 2002. It wasn’t long before journalists and activists who assist the poor began hearing similar tales of woe:

I didn’t know that the small loan had such hidden, expensive interest rates. The fees and interest are higher than the amount of the original loan. When I don’t pay, companies or their collection enforcers keep calling at home and work, demanding cash.

Here’s what Lisa Gibbs of Spotsylvania told the Virginia Poverty Law Center, in comments later forwarded to federal consumer advocates in 2019. She had gotten a loan for dental work:

“Even though the loan was for only $1,500, the interest rates grew until I owed more than $5,000,” Gibbs said. “This loan has done lasting damaging to my credit score, and to this day I am struggling to get approved to buy a house.”

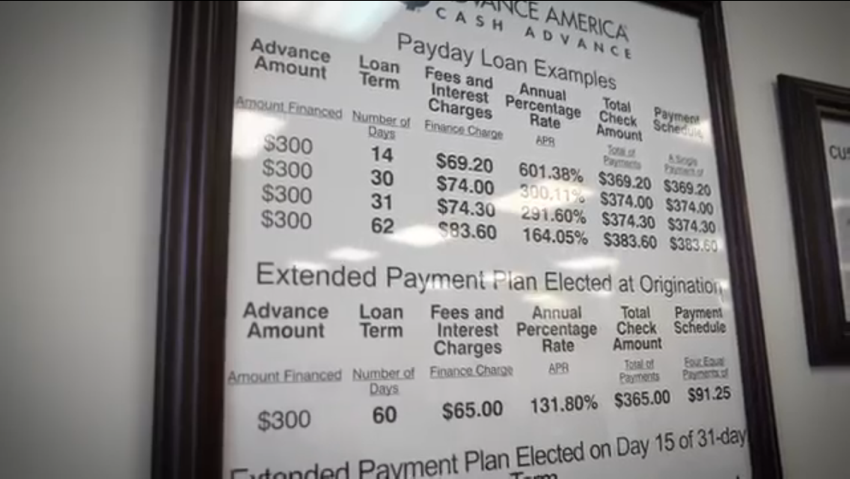

Early on, the annual percentage interest rate the companies charged approached 400 percent! Loan sharks would’ve coveted the legal protections outfits like Advance America and Title Max enjoyed.

The industry had contributed generously to some state legislators. Before this year, bills to get tough on lenders often died each Assembly session.

According to a recent Daily Press article, payday loans are secured by a post-dated check for a higher amount. Surcharge and interest that lenders have been allowed to assess meant the equivalent of “an annual interest rate of as much as 818 percent, Bureau of Financial Institutions data show.”

“Title loans are secured by the borrower’s car or truck, which means that if the borrower misses a payment, the lender can take the vehicle,” the Daily Press reported. “These lenders had been allowed to charge interest rates of up to 268%, bureau data show.”

State records reveal that in 2018, car title lenders repossessed 14,105 vehicles in Virginia. That means people lose their main means of transportation.

The rules will change Jan. 1, when interest for both types of loans will be capped at 36 percent. Payday lenders can charge a monthly fee of up to $25, and car title lenders a monthly fee of up to $15.

The new regulations had bipartisan support.

This result didn’t sit well with Advance America, which announced on its website: “The state of Virginia recently passed a law that limits our ability to operate and, as a result, we are closing our stores.”

Guess when the game isn’t rigged as much as you’d like in your favor, you pout.

“Other states like Ohio and Colorado have similar regulatory models, but lenders, including Advance America, have been challenged to find success with those products under overly restrictive laws,” Jessica Rustin, Advance’s chief legal officer, told me by email. “That experience, coupled with Virginia’s existing burdensome unencumbered cash requirements for licenses, contributed to the company’s decision to exit its operations in Virginia.”

However, Jay Speer, executive director of the poverty law center, told me there’s still plenty of incentive for these firms to make money. It’s just that several loopholes are now closed.

“We put this bill in and had a lot of research and facts behind it from the Pew Charitable Trust,” he said. The result is a fairer process for lenders and borrowers.

It might still be tough for low-income people to obtain small loans in an emergency. Banks and other financial institutions aren’t doing enough to make money available.

But what the Assembly approved is progress, if not as harsh a measure as in other places. Many states don’t even allow car title lenders to operate. That’s perhaps one reason why the commonwealth is a magnet for some of these companies.

So Advance can get all in a huff if it wants to. Here’s a suggestion:

Don’t let the door hit you on the way out. – Virginia Mercury

Chesley is a longtime columnist and editorial writer who worked at the (Newport News) Daily Press and The (Norfolk) Virginian-Pilot from 1997 through 2018.